Understanding Contango and Backwardation

In the realm of commodity markets, the terms contango and backwardation are pivotal, describing the futures pricing structures in relation to current spot prices. Investors, traders, and market analysts utilize these concepts to assess market conditions and future price expectations. Understanding both can give a clearer insight into the underlying mechanics of commodity trading and the expectations around supply and demand dynamics.

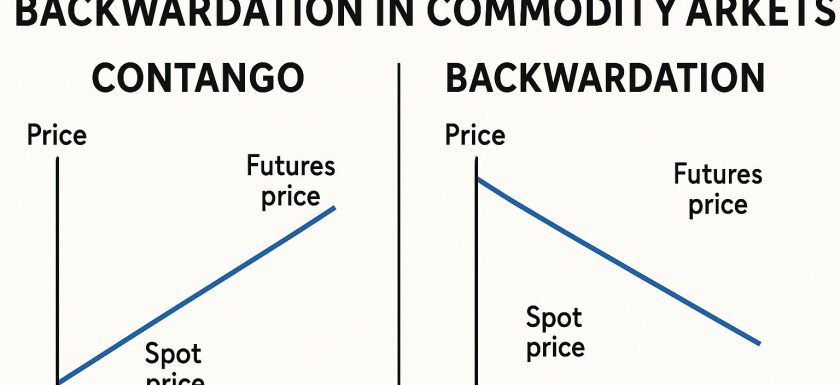

What is Contango?

Contango is a term used to describe a market condition where the futures price of a commodity is notably higher than the expected future spot price. This pricing structure reflects investor expectations of price increases over time, generally due to various factors such as storage costs, the time value of money, and other associated carrying expenses. In a contango market, prices for futures contracts tend to decrease as they approach their maturity date. An investor choosing a longer-term contract often justifies the higher price with the anticipation of future gains outweighing the initial premium.

In practical applications, contango is often observed in markets with an abundant supply of the underlying asset. For instance, when there is an excess of oil, the cost of storing surplus barrels leads to higher future prices. As maturity nears, the carrying costs reduce, leading the futures price downward to align with current spot prices.

Effects of Contango

Increased Carrying Costs: Contango situations reflect storage and other carrying costs through the price differential between the futures price and the spot price. Traders incorporate these expenses when evaluating futures contracts.

Speculative Behavior: The anticipation of price changes can drive speculative activities. Traders might take positions based on their market predictions, contributing to trade volume and market liquidity. Speculative trades often serve as a mechanism to express views on future market conditions.

What is Backwardation?

In contrast to contango, backwardation describes a market condition where futures prices are lower than current spot prices. This typically signifies market expectations of declining prices in the future. Such a condition often emerges amidst concerns over future supply shortages or an immediate deficit impacting the current availability of the commodity.

In a backwardation scenario, the spot price tends to trend downward toward the futures price as the contract nears maturity. This market environment can prompt traders to prioritize holding the physical commodity instead of purchasing futures, anticipating that current high prices will ease. Essentially, backwardation reflects a high demand versus an immediate supply shortfall.

Implications of Backwardation

Higher Demand: Backwardation can be an indicator of heightened demand or impending supply limitations, often signaling tight market conditions where immediate access to the commodity is prioritized.

Inventory Drawdown: In a backwardated market, businesses and traders might choose to deplete existing inventories rather than acquiring futures at elevated spot prices. This behavior can affect inventory levels significantly, impacting supply dynamics and influencing market pricing further.

Factors Influencing Contango and Backwardation

The state of a commodity market—whether it is in contango or backwardation—is influenced by several critical factors, each having the potential to sway market behavior and pricing structures significantly.

Supply and Demand Dynamics: Fundamental supply and demand conditions are primary drivers of contango and backwardation. An oversupply situation often supports contango, while supply constraints tend to result in backwardation. Market participants closely watch these dynamics to gauge potential price movements.

Storage Conditions: The availability and cost of storage play a part in the price formation of futures contracts. When storage costs are high, futures prices may increase to reflect these expenses in a contango market. Conversely, limited storage access can contribute to backwardation.

Economic Indicators: Broader economic indicators, including inflation expectations, interest rates, and currency fluctuations, can influence futures pricing. Economic trends shape market sentiment and are considered by traders when evaluating the likelihood of a market being in contango or backwardation.

Conclusion

Both contango and backwardation offer critical insights into the anticipations of investors and traders in commodity markets. By understanding these conditions, individuals and businesses can craft more informed strategies when engaging in futures markets. The ability to interpret contango and backwardation can provide a more nuanced perspective on future supply and demand conditions, ultimately leading to more strategic decision-making concerning price expectations.

Investors and analysts seeking a more comprehensive understanding can delve into detailed studies available through specialized financial literature. This deeper exploration can enhance strategic approaches within commodity trading, offering refined methods to anticipate and respond to market shifts. Understanding these dynamics remains vital for stakeholders looking to navigate the complexities of the commodity markets effectively.

This article was last updated on: October 17, 2025